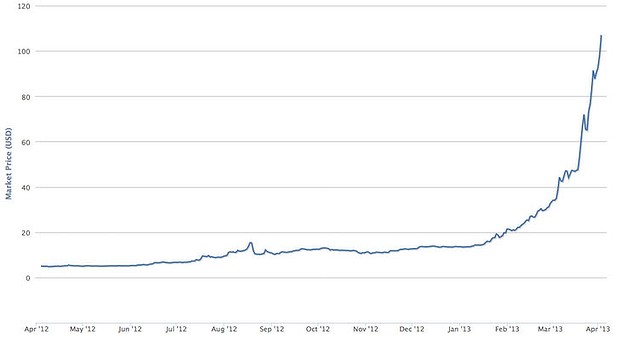

Nations around the world are flexing the powers of their central banks, from open-ended quantitative easing in the US, to Greek bailouts in the Eurozone. This top-down approach is stretching dangerously thin, both in scope and in effectiveness. One emerging contender to upend the locus of control is Bitcoin, which demonstrates a way to decentralize this authority by sidestepping the fiscal monopolies of individual governments. The demand for Bitcoins has risen dramatically in the past few months, currently trading at well over $100 per coin, as people see a potential escape hatch from traditional currencies. There is now more than $1 billion worth of Bitcoins globally, more than the entire currency stock of 20 countries.

Bitcoin is an online and anonymous currency that can be used to make global transactions. Unlike similar services such as PayPal, the servers that support Bitcoin are distributed across the world, which makes it impossible, or at least very difficult, for governments to shut down. Bitcoins can also be used to purchase traditional hard currencies like dollars, euros or yen. These advantages are making the service an attractive way for people to secure money – almost likened to a digital, mobile version of squirreling gold away in a shoebox.

People are becoming more interested in a monetary safe haven, especially considering the recent events in Cyprus. In mid-March, the European Union and the International Monetary Fund penned a deal that rightfully incensed Cypriots and sent ripples of fear throughout international markets. In exchange for a €10 billion economic flotation device, the agreement stipulated that accounts in the two largest banks in Cyprus would be given a haircut: a 6.75% confiscation of amounts under €100,000 and a whopping 9.9% for accounts holding more.

The Cyprus legislature rejected the deal. However, on March 25, Cyprus President Nicos Anastasiades, along with Eurozone and IMF officials, announced a new plan (which didn’t require parliamentary approval) that would preserve the tax on amounts of more than €100,000 but not on those with less. An estimated 40-80% of the value of such top-tier accounts could be lost. As many of these are held by wealthy Russians who use Cypriot banks as a tax-haven, this compromise seems to be an example of shortsighted and naïve thinking: “Well, it’s not our money being stolen, so it’s OK this time!”

Upon hearing the news, many Cypriots wanted to withdraw their savings to avoid the automatic deductions. However, the government simply closed banks for 12 days, eliminating that avenue of escape. Upon opening them again, withdraws were limited to €300 a day per customer, with some locations lowering the maximum to €100. Anyone leaving the country may only take €1,000 in cash with them. There also restrictions for how much money can be sent overseas.

This is one example of why Bitcoin is becoming so popular. These drastic and draconian measures that hope to ensure solvency are likely attractive to myriad nations facing economic stressors, the US included. Bitcoins can’t (yet!) be confiscated or shut down and they can be used by anyone, anywhere, for any reason. The anonymity the service provides also helps ensure that itchy government fingers–jonesing for their next fiscal fix!–can’t simply swipe money from Bitcoin owners.

People like Charles Schumer (D-NY) and the Drug Enforcement Agency decry Bitcoin for its utility in circumventing federal laws. This is completely irrelevant, as regardless of its form, money has always and will always be used for funding of any kind, illicit or otherwise. Their outrage is based on the idea that somewhere there is activity that they cannot control. Anything that unnerves moral busybodies is a net positive and is further reason to support crypto-currency. People own the fruits of their labor and anything that helps keep the government from snatching it away is something to be lauded.

Bitcoin and other digital currencies are certainly nascent technologies prone to error. With the rapid increase in Bitcoin’s value, it has been speculated that the entire enterprise is a rapidly inflating bubble. The value has skyrocketed since early March, from $35 a coin to $145 on April 2. I wouldn’t be surprised if the theorized balloon eventually bursts, but I think the collapse would be due to its relatively recent emergence into the market rather than any inherent flaw in the currency. It takes time for new industries to fully adapt to its environment and clientele—just look at the Internet—but that doesn’t mean that the technology is unwanted or not revolutionary.

More than just Bitcoin, I am enamored with the idea of state-less money and better, safer ways for people to preserve their labor free of government intervention. I welcome increased competition in the crypto-currency market, which would help weed out design flaws, increase stability and ensure that users are as satisfied as possible. It would help individuals retain autonomy over their money, which is considerably better than the current central bank system, which either directly taxes wealth away or decreases its value more subtly through inflation.

Anything that helps maximize individual liberty is a good unto itself, and the cynic in me derives otherworldly pleasure from helping to deprive governments of the unjust ability to impose their will upon the unwilling. Bitcoin may not be perfect, but it’s a step in the right direction towards financial autonomy.

That’s a fiscal revolution worth celebrating.

Sources:

http://www.bbc.co.uk/news/world-europe-21819990

http://www.guardian.co.uk/business/2013/mar/28/cyprus-reopen-banks-stock-market-closed

http://www.fincen.gov/statutes_regs/guidance/pdf/FIN-2013-G001.pdf

http://www.reuters.com/article/2011/06/08/us-financial-bitcoins-idUSTRE7573T320110608

http://www.businessinsider.com/im-raising-my-bitcoin-price-target-to-400-2013-4